It can be imperative to know how to check your credit score, in the event of a loan. Almost every single lender out there performs a credit score check when you apply for one of their finance options. They do this to be able to tell just how reliable you are in paying back the sum of money they’re about to lend you. Therefore, a good idea would be to stay ahead of the game and know how to check your credit score yourself, in case you need to work on it. Here are a few ways of doing that.

How to Check Your Credit Score

As mentioned in the introduction the main reason you will want to do a credit score check is to stay one step ahead of all your potential lenders. The credit score is, in fact, a sum of points you are granted for your past financial behavior. If for example, you have unpaid installments from other loans or mortgages, they will decrease your credit score. The same goes for unpaid bills or rent.

Another thing that will take its toll on your credit score and that you need to pay attention to is the application for a loan in itself. This is one thing that many people don’t, in fact, realize is happening. Whenever you apply for a loan of any kind, from store credit cards to buy furniture, for example, to mortgages and other large amounts of money, the lender has to check your credit score. Whenever they do, it drops a few points. It might not seem like much taken independently, but put it in perspective and you’ll notice you may have even lost 100 points solely from that.

Taking all this into consideration, it becomes crucial to know how to check your credit score yourself, just in case you have to work on it. Here are four easy ways to do that.

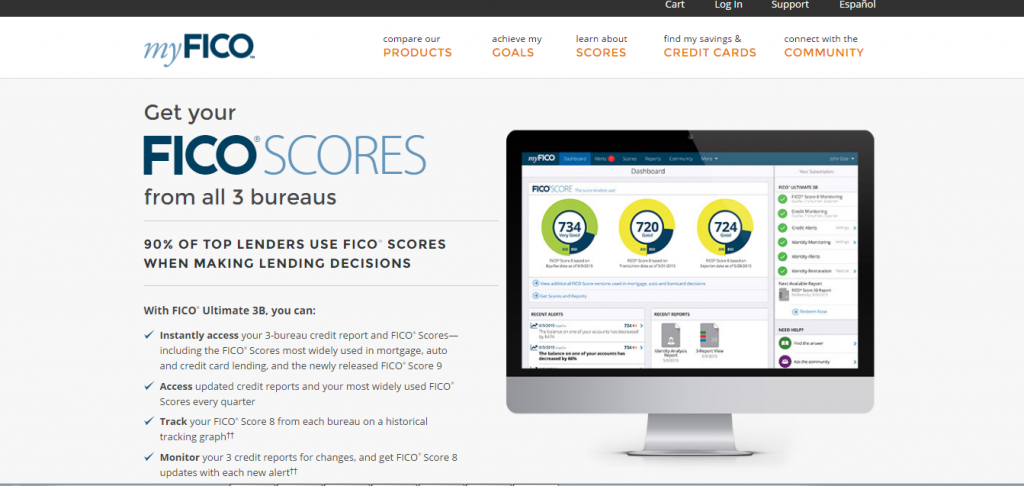

#1. Using FICO

FICO is otherwise known as the Fair Isaac Corporation, and its credit scores have become a staple in the world of finances and lending. The corporation is the one who develops the famous FICO scores and maintains them as well. You can head over to their dedicated page, myfico.com and get yours.

One thing you need to know before going to the website is that the services are not free. You have to pay $29.95 per month, a subscription which will renew itself automatically unless you cancel it. They may offer you a 10-day trial period when you sign up. Apart from that, you also have to create an account with them to see your credit score.

We listed FICO as the number one way on how to check your credit score because, since it’s used by the best part of lenders who offer instant approval, it has become the gold standard of credit scores.

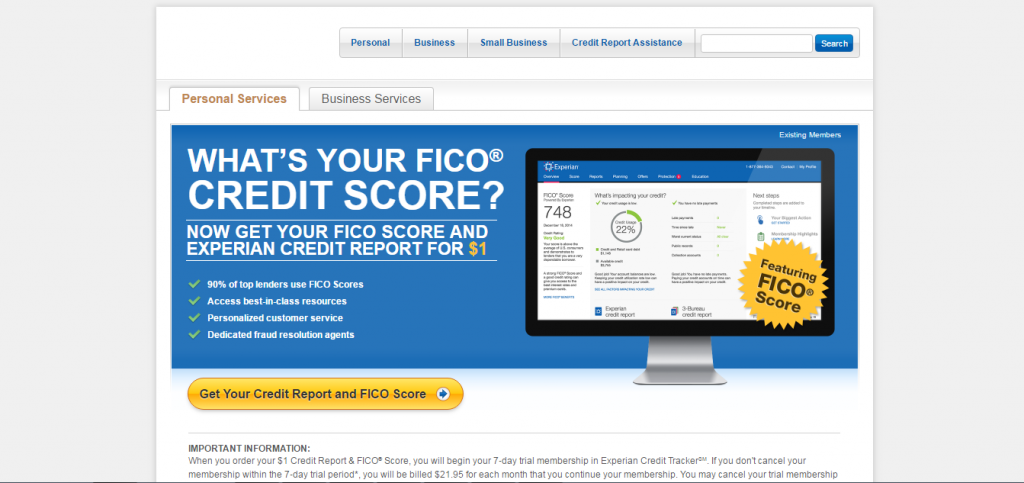

#2. Contacting the Credit Bureaus

There are three major credit bureaus in the United States.

You can go to their websites and purchase a report that shows your complete and detailed credit score. However, you need to know that you will have to answer a series of questions before you are allowed to do that. Seeing as your credit score is confidential information, these websites will ask you for personal details that only you may know about yourself. For example, they might ask you to fill in your social security number or details related to your mortgage payment.

Upon applying, you will also need to provide your credit card info. The reports are what they call a ‘3-in-1’ format. This means that when and if you apply for one of them, you will get all three. However, this is a two-way street. It is a good idea to get all three scores, but you will be paying for all of them as well.

#3. Credit Monitoring Services

How to check your credit score is easy if you want to go for the credit monitoring services option. These are websites that allow you to track your score and how it changes over the course of a month. They will ask for a monthly fee, just like all the other options. However, they might not be the best idea if you just want to apply for a loan.

When you do, you will only need to know your credit score that one time or for a limited period, until they grant you the loan. A monitoring service is better suited for people who have been the victim of identity theft or who merely want to watch their score on a permanent basis.

You can monitor your credit score on the MyFico.com website, as well as with the bureaus. There are also some third-party sites that offer this service. Even so, you need to make sure they are legal and authorized before you enter your personal financial data in their systems. They usually allow you to check your score once a month. Some of them update on a monthly basis while others update in real time and notify you about any changes that occurred.

#4. The Annual Free Credit Score Report

The website you need to use in this case to learn how to check your credit score is annualcreditreport.com. Thanks to the Fair Credit Reporting Act, every person in America is entitled to receive a free credit report every single year from all the major credit bureaus in existence. There are three ways to ask for it.

- Log onto the website and complete the online form

- Call 1-877-322-8228. This number doesn’t pertain to any of the bureaus directly since you don’t need them for the report itself. However, you will need them for the credit score, for which you will have to pay.

- Send a letter to the following address – Annual Credit Report Request Service, P.O. Box 105281, Atlanta, GA 30348-5281. You need to enclose in the envelope the Annual Credit Report Request form. You can download it from the FTC website.

When you apply, you need to be ready for a plethora of questions, such as the following.

- How many mortgages and loans you have applied for and been granted so far

- All your credit card info

- Very personal questions, such as how many bedrooms your house has

- Trick questions – asking for mortgages even though you never applied for one or giving you unrealistic choices when asking the ‘how many bedrooms’-question.

One crucial piece of information which you must know is that the report does not contain your credit score. You will need to follow the above courses of action for receiving it.

Getting to know how to check your credit score is easy enough. It usually involves you accessing a website, calling a particular phone number or mailing a form to the authorities. The only thing that stands between you and the information is the fact that these are not free services. However, seeing as your credit score is considered crucial information don’t be afraid to spring for that extra cost.

Leave a Reply